What Is Credit Card Processing?

Credit card processing is the ability to accept credit and debit cards in person, over the phone, or via mail order through a payment provider that can securely process each transaction. A Credit Card Processor offers services that ensure the customer can make transactions using credit and debit cards simply for quick checkouts.

What Is The Process When Accepting Credit Cards?

The process begins when a customer provides their payment details, whether it’s:

- In-person using a card reader at a Point Of Sale (POS) or a terminal

- Online using an e-commerce store’s hosted payment form

- Over the phone or mail.

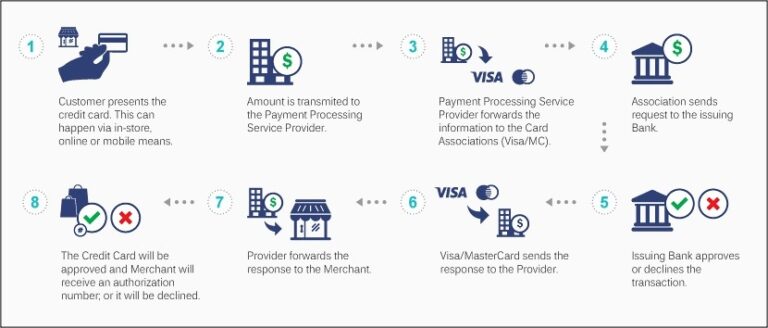

Who Are The Key People Involved in Credit Card Processing?

1. The Customer: The initial stage in credit card processing begins when a cardholder swipes their card or provides their payment information to the merchant.

2. The Merchant: The merchant accepts and collects the payment information in one of two ways: Physically, by accepting payments from the cardholder referred to as Card Present Transactions and through online transactions referred to as Card Not Present (CNP) Transactions processed through a gateway that collects the payment from the customer.

3. The Processor: The credit card processor collects the payment information and is responsible for routing that data across various stages as well as facilitating communication between various parties.

4. The Card Network: The customer’s card will operate through one of the major credit card provider’s networks such as Visa and MasterCard. After the information has been received from the processor the customer’s card network will then relay it to the customer’s bank.

5. The Customer’s Bank: The cardholder’s bank receives the payment request and verifies whether the cardholder has sufficient funds to complete the purchase. If the cardholder has insufficient funds the bank will deny the transaction.

6. The Merchant: Provided that the transaction is cleared, the merchant is expected to provide the customer with the goods and services purchased.

It is important to note that at this point no funds have actually been released yet. Meaning the transaction is not completely settled. Depending upon the customer’s card network, the time period may vary to settle the funds. The process of settling and releasing the funds from the cardholder’s bank to the merchant’s bank involves the same process as described above.

The Current State of The Credit Card Processing Industry

Between technological advances and the preference of mobile payments by millennials and Gen Z, the credit card processing industry is changing daily. However, despite the rapidly evolving payment options that consumers have today, credit cards remain the leading payment method.

Millennials & Gen Z Consumers

Millennials and Gen Z consumers are disrupting the credit card processing industry by favoring different forms of payment. Although, most millennials own at least one credit card according to a survey conducted by Bankrate. They also state that older millennials (ages 30-38) have more credit cards than any other age group.

Replacing Old Ways With New Ones

Instead of swiping credit cards or manually entering a customer’s credit card information, merchants should be looking to new and exciting ways to process payments.

Popular mobile wallets, such as Apple Pay and Samsung Pay rely on NFC technology which allows customers to make purchases simply by holding their phone to a credit card terminal, reducing the amount of time the customer spends in the checkout line and allowing merchants to accept more customers.

Since many mobile wallets require two-factor verification, processing payments in this method is highly secure. For merchants, receiving mobile wallet payments is fast and affordable.

All-In-One Cloud-Based Payment Processing Systems

Companies like Merchant Industry understand the changes and advancements being made in the payment processing industry and offer multiple processing options to make our merchants more efficient in a competitive market. That’s why we have created all-in-one processing services that enable merchants to process credit cards online as well as provide the ability to track sales, inventory, and employee performances. Since all of this information is on the cloud it can be easily accessible from anywhere and at any time at the convenience of the merchant. Learn more at Merchant Industry.

The Future of Credit Card Processing

Both the customer and merchant expect payments to be processed quickly and conveniently. In fact, businesses around the world have already stopped accepting cash payments according to The Wall Street Journal. As more and more people continue to manage their funds electronically and synchronizing their cards to their mobile devices, the credit card processing industry is swiftly moving towards contactless payment methods that are not only convenient, but also secure thanks to techniques like encryption, tokenization, and biometrics. All of which Merchant Industry provides.